The battery revolution was supposed to change the world. Then reality hit.

Between 2020 and 2022, investors poured tens of billions into battery startups. By 2024, investment in the sector had collapsed 39%. Here’s what I witnessed.

I worked at a Northvolt subsidiary. And I watched the entire company fall apart.

When I joined, the mission felt invincible — almost how the people boarding the Titanic felt. This was the unsinkable ship. Peter Carlsson, a former Tesla executive, co-founded the company in Stockholm in 2016 with a single, audacious goal: build the world’s greenest battery and give Europe its own answer to Asian battery dominance. It wasn’t just a startup pitch; it quickly became a global climate movement.

By every external measure, Northvolt looked like it was winning. The company raised nearly $13 billion in debt and equity, locked in over $50 billion in battery orders from major automakers, and was hailed as the flagship project of Europe’s green industrial reinvention.

Then, the first set of cracks started to form. BMW canceled a €2 billion contract in June 2024 due to production delays. BMW was losing faith in Northvolt’s ability to get things done. Shortly after, on November 21, 2024, Northvolt filed for Chapter 11 bankruptcy in the United States. By March 2025, it had filed for bankruptcy in Sweden. It was the largest bankruptcy in Swedish history.

The company had originally planned its flagship plant, Northvolt Ett, to reach 60 GWh of annual capacity. By the time it filed for bankruptcy, it had scaled that ambition back to 16 GWh, which was the same target it had set in 2017. Years of investment, and they were back at the starting line.

At the time of filing, the company carried $5.8 billion in debt. Ultimately, all 6,600 workers across seven countries lost their jobs. Several talented colleagues of mine had their lives shaken, struggling to find footing again in an industry where very few companies were hiring.

Employees at Northvolt drank the Kool-Aid. I was one of them. I had already left before the filing, but I hadn’t walked away clean. I’d invested a significant amount because I believed in it. Watching it collapse from the outside, knowing the people still inside and knowing what I’d personally put on the line, was something between grief and a hard lesson.

Northvolt didn’t fail quietly. But it also didn’t fail alone.

A Graveyard of Good Ideas

The battery and EV space was, for a few years, the most exciting investment frontier on earth. Venture capital flooded in and governments cheered. Automakers signed multi-billion-dollar contracts. The energy transition felt not just inevitable, but imminent.

Then the companies started dying.

Natron Energy. Ambri. Powin Energy. XALT Energy. Moxion Power. Li-Cycle. Britishvolt. Proterra. Alelion Energy Systems.

These weren’t fringe operations. They were well-funded, well-staffed, and well-intentioned companies trying to build the infrastructure of a clean energy future. And yet, when you look closely at how each one unraveled, the same undertones keep surfacing.

Planning a battery revolution without planning the build — Li-Cycle raised $1.7 billion to build North America’s first large-scale battery recycling facility. Construction costs nearly doubled from original projections and in October 2023, construction halted entirely. By May 2025, the company filed for bankruptcy, and Glencore acquired all assets for $43.6 million. They began construction before they knew what it took to get it done. The factory never ran.

Building the factory before having customers — Britishvolt announced a £3.8 billion gigafactory with 3,000 jobs and zero binding customer agreements. They raised £200 million from private investors and secured a £100 million pledge from the UK government before a single cell was ever produced. That’s crazy to even think about. They built a brand and somehow got funding before they built a business. Talk about putting cart before the horse.

Trying to manufacture everything but mastering nothing — Proterra was one of the more mature companies in the space, focused on electric buses. But then it tried to scale electric buses, batteries, and charging infrastructure simultaneously. They had real traction in the electric bus market, with over 600 buses delivered to transit agencies across North America. But instead of doubling down, they wanted to diversify. The part of the business that should have been the foundation became an oversight while their attention was split between several other business areas.

Betting everything on one supplier — Powin’s entire business model was built on importing Chinese LFP cells and integrating them into storage systems. Their cell suppliers were all Chinese manufacturers and they had no alternative supply chain in place. When tariffs hit 40%+ and threatened to go higher, the cost model snapped. In fact, they knew the dependency was not going to work long-term, but built on it anyway. That’s not a supply chain strategy, that’s a liability.

Racing to scale without UL certification — Natron Energy developed sodium-ion batteries with genuine promise, then made a classic sequencing mistake: they planned to build a 1.2 million square-foot plant before regulatory certification was secured. When investor payments froze pending UL certification approval, operations halted. Going to market and trying to scale without locking in the regulatory foundation first is a critical planning failure.

These were not isolated failures; they were symptoms of something much larger.

The Manufacturing Gap Nobody Wanted to Admit

At the core of almost every failure in this space is a single, underappreciated problem: building a battery company that can compete with the behemoths in Asia is nothing like building a tech startup. But from where I sat, they definitely tried to spin it that way.

Developing groundbreaking battery technology doesn’t come easy and neither does building it at scale. Physics doesn’t “move fast and break things.” Yield problems, thermal management challenges, and materials consistency issues don’t respond to sprints and agile methodology. You either have manufacturing discipline baked into your DNA from day one, or you spend billions discovering you don’t.

These companies were short-sighted. They had a great idea and thought that they could get by riding the VC wave. They thought hiring the best scientists and brightest battery minds would attract more money and get them over the finish line. But it didn’t. The talent was there, sure. They had world-class chemists, engineers, people who understood the science. But the deep technical knowledge and the ability to properly plan, scale, and grow a battery business are two different things. You can have the smartest technical people in the room and still have no idea how to plan a factory floor, launch a commercially viable product, or prove you can do any of it at scale.

That’s what nobody wanted to say out loud. Northvolt was the prime example of this. To become competitive and keep costs down, your product has to be manufacturable at scale. They definitely showed they can build the giant space capable of housing it all, but they didn’t approach it properly.

They announced several accomplishments that appeared to be true success, but there were serious foundational and strategic problems bubbling beneath the surface. I remember hearing about how the equipment wasn’t capable of achieving the throughput required and how they continually had quality issues. They started building a gigafactory before they solidified their processes. Proving out process comes first, large capital expenses come next. Instead, they decided to build the factory, buy the equipment, hit the milestone (on paper), and figure it out later. But moving a status bar on a Gantt chart is not progress, it’s theater. And it was a very expensive lesson learned for all those who invested in them.

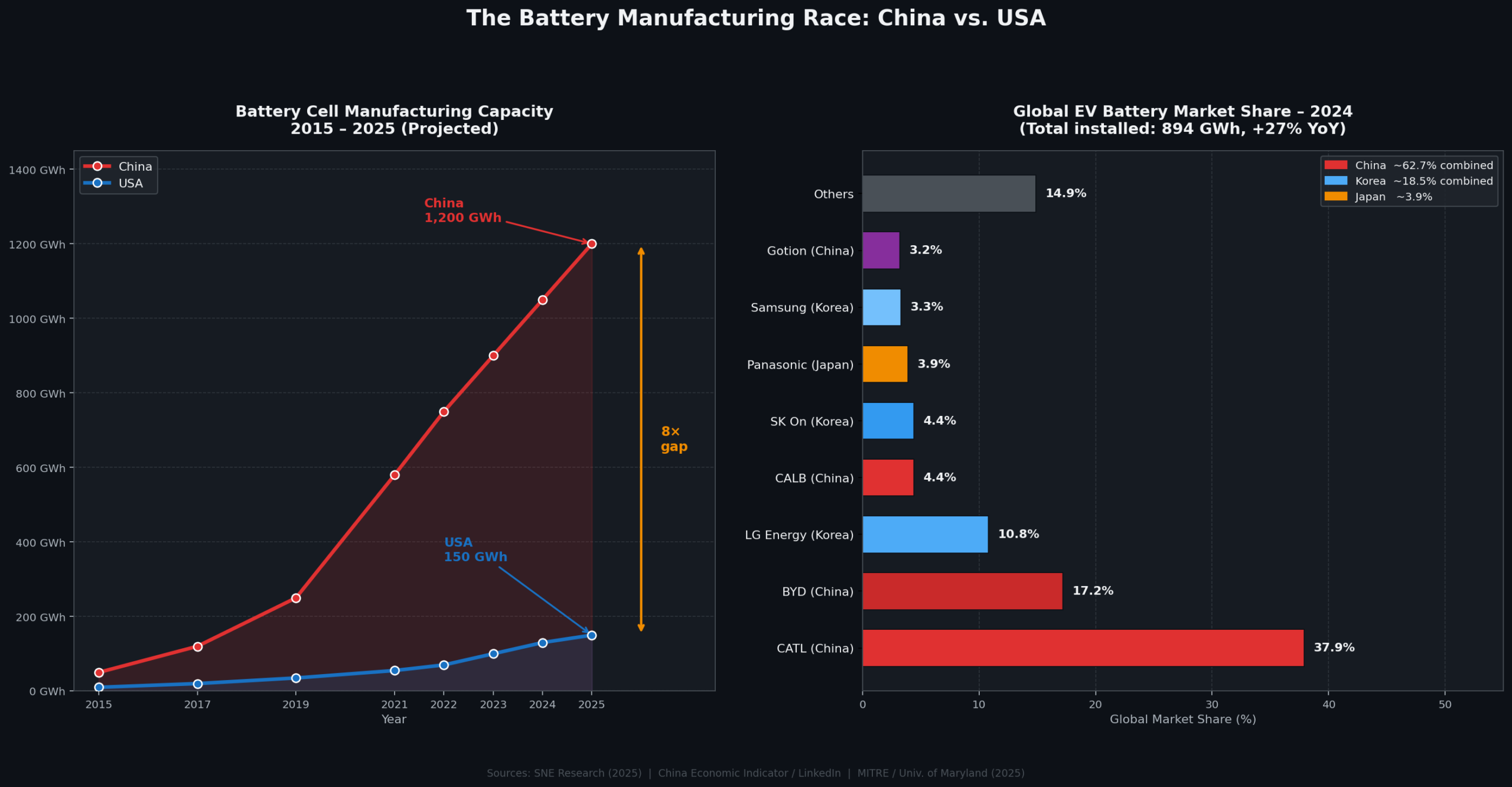

China, South Korea, and Japan didn’t build their battery manufacturing dominance with bold vision decks and VC funding rounds. They built it over decades, through relentless iteration, state-backed capital, and supply chain integration that runs from raw material extraction all the way to the finished cell.

CATL alone now holds 39.2% of the global EV battery market. They are the only manufacturer in the world with more than a 20% share, and grew that position by 35.7% in 2025 alone. Combined, CATL and BYD now control 55.6% of global EV battery supply. China as a whole controls 68.9% of the entire global EV battery market.

Western companies weren’t competing with other startups. They were green knights challenging a Kingsguard with 30 years of experience.

The cost calculations alone tell the story. Building a 1 GWh battery manufacturing facility costs approximately $55 million in China and $100 million in the United States. Manufacturing in the U.S. runs about 16% more expensive than simply importing from China, even before factoring in supply chain, energy, and labor overhead. European cells from companies like Northvolt were priced as much as 90% higher per kWh than Chinese best-in-class manufacturers. You cannot compete on those economics by willing it away. You need time, scale, and a realistic plan to get there. The problem is that most of these companies had none of those three things in the right proportion.

The capital dried up because trust was lost. The confidence in competing with Asian countries to scale new technologies and gigafactories in the West was gone. In a capital-intensive industry, once that confidence is gone, everything else follows.

What the Companies Couldn’t See

1. Capital Without Milestones is Death by 1,000 Papercuts

The battery space attracted enormous capital, but capital alone cannot replace decades of manufacturing and strategic planning experience. Companies kept returning to investors with the same message: we’re almost there, we just need more runway. Eventually, investors stopped believing it. Many of them have absorbed nine-figure losses. Goldman Sachs alone is expected to absorb a $900 million loss from its Northvolt position.

2. Leadership Hubris Filled the Gaps Capital Couldn’t

When you have a world-changing mission and a roster of blue-chip backers, it is dangerously easy to confuse ambition with execution. Several of these companies were led by people who had never built a factory before, let alone tried to compete with manufacturers who had been refining their processes for 30 years. The vision was real. The operational rigor, in many cases, was not. In Northvolt’s case, co-founder Peter Carlsson stepped down as CEO the same day bankruptcy was filed. It was the end of a leadership era that, despite ambition, could not bridge the gap between what the company promised and what it could actually deliver.

3. The Technology Horse Race

If the manufacturing problem is about execution, the technology problem is about proliferation. Right now, the battery industry is simultaneously pursuing solid-state, sodium-ion, lithium-metal, lithium-sulfur, lithium-air, semi-solid-state, and iron-air batteries — each championed by different companies, research institutions, and investors as the definitive solution. The truth is that all “beyond lithium-ion” technologies combined are projected to capture only about 15% of the market by 2029. Most horses in this race don’t finish. Spreading investment thinly across too many unproven chemistries while Asian manufacturers scale is about as much a strategy as throwing dust to the wind.

4. Government Incentives Came Late and Are Now Under Threat

The U.S. Inflation Reduction Act was a meaningful step. Since its passage, nearly $100 billion in private-sector investment has been announced across the domestic clean vehicle and battery supply chain. The Advanced Manufacturing Production Tax Credit was specifically designed to make U.S. battery production cost-competitive globally. But the incentives arrived years after the investment had already flowed into companies that were structurally unequipped to use them effectively, and the current political climate puts even these programs at risk. Policy cannot rescue a factory that was never built right in the first place.

5. Infrastructure Was Never Ready and Policy Ignored That

California’s Advanced Clean Cars II regulation mandates that all new passenger car sales be zero-emission by 2035. It was an ambitious policy, and arguably the right long-term direction. But the U.S. Senate voted in May 2025 to block it, and the practical arguments for doing so are not entirely unfounded. The United States currently has approximately 230,000 public charging connectors in operation. The Department of Energy estimates the country needs 1.2 million public chargers by 2030 to support projected EV adoption levels. We are building the runway while the plane is already supposed to be in the air.

This isn’t an argument against EVs but rather an argument that policy ambition, manufacturing capacity, and infrastructure investment must move together. But in this case, they never did.

What Comes Next

The battery revolution is not dead. Much of the technology still being developed shows promise and the climate need is urgent. The companies that survived the shakeout or the new ones being built today may ultimately deliver on what the last generation promised.

But the era of betting on vision alone is over. The survivors will be the ones who treated manufacturing as the product, not the afterthought. They’re ones who understood that you can’t outspend decades of experience and that failure is not inevitable even with billions of dollars in the bank. What is the old adage? Proper Planning and Preparation Prevents Piss Poor Performance. I hate to sound cliché, but it’s true!

I watched Northvolt get cocky and fall short. I believe the next generation of builders can do it differently.

The question is whether the capital, policy, and patience will be there when they do.